In May 2014, the FASB issued Accounting Standards Update (ASU) 2014-09, Revenue from Contracts with Customers (Topic 606). Since then, there have also been several amendments to the ASU that provide clarification to the original guidance. The update will be effective for all nonpublic entities for reporting periods beginning January 1, 2019. The core principle is that an entity should recognize revenue based on what is being exchanged and when.

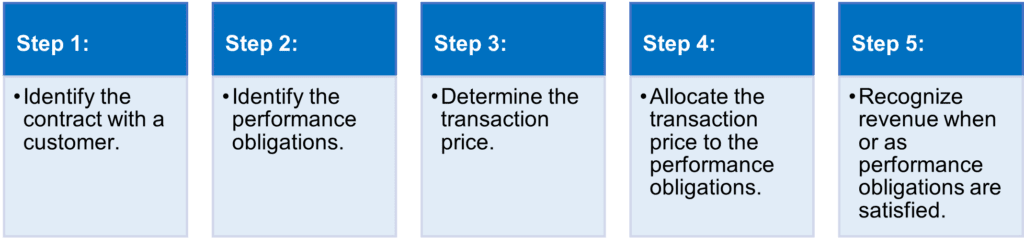

This is established by a five step approach:

Step 1: Identify the Contract with a Customer

The application of this step will be straightforward the majority of the time. The contract or agreement will follow this guidance if the following criteria are met:

- Approved contract by both parties – Written or oral

- Each party’s rights can be determined – Who’s doing what

- Payment terms are identified – How much

- Commercial substance exists – The transaction is worth something

- Collection is probable – You will get paid for the sale

Step 2: Identify the Performance Obligations

This step identifies what’s being delivered or provided to the customer. This is one of the more significant changes because a contract can have more than one performance obligation, and each obligation will need to be specified. Another way to think about it is to consider if the customer can use or benefit for the good or service on its own. If they can, that is probably a separate performance obligation. For example, a customer enters into an agreement to buy equipment with a year of free maintenance. There are two distinct performance obligations – The sale of the equipment and the year of maintenance.

Step 3: Determine the Transaction Price

When determining the price, there are a few things to consider and their effects:

- Variable Consideration – Estimated amount received after rebates, discounts, refunds, etc.

- Financing Component – Time value of money consideration if there is a financing component.

- Non-Cash Considerations – Items provided should be measured at fair value of what is received.

- Amounts Payable to Customer – In the contract, if anything is owed to the customer, the transaction price should be reduced by that amount.

Step 4: Allocate the Transaction Price to the Performance Obligations

If there are multiple performance obligations, the transaction price must be allocated to each performance obligation on a relative standalone basis. The best way to do this is to compile each performance obligation’s standalone price if it were sold separately by the entity. If a standalone selling price is not directly observable, it must be estimated. Combine the standalone selling prices and allocate the transaction price proportionately to each performance obligation based on their respective standalone prices.

Step 5: Recognize Revenue When or As Performance Obligations Are Satisfied

Revenue will be recognized as the performance obligations are completed and control of the good or service is transferred to the customer. Control is considered to be transferred when the customer has the ability to direct the use of and receive benefit from the good or service. In a retail environment, control is transferred upon the selling of the good, and revenue would be recognized at that time. If the performance obligation is transferred over time, like in a one year maintenance contract, revenue will be recognized over the year as the performance obligations are completed.

Additional Disclosures in the Financial Statements

The ASU will also result in new disclosures in the financial statements. Nonpublic companies will be required to disclose information about all of the following:

- Its contracts with customers

- Revenue recognized from contracts with customers

- Disaggregated revenue into categories that depict how the nature, amount, timing, and uncertainty of revenue and cash flows are affected by economic factors

- Contract balances for opening and closing balances of receivables, contract assets, and contract liabilities

- Method(s) used to recognize revenue for performance obligations satisfied over time

- Significant judgments, and changes in judgments, in applying the guidance

- The timing of satisfying performance obligations

- Determining the transaction price and allocating amounts to performance obligations

- Any assets recognized from the costs to obtain or fulfill a contract with a customer

The above information presents some, but not all, of the changes resulting from the new accounting standard. If you have questions on how the update will specifically affect your business, please contact your Wegner CPAs professional.