How to Report DAFs on Form 990

Donor Advised Funds (DAFs) have become a popular tool for charitable giving, allowing donors to contribute assets, receive an immediate tax deduction, and recommend grants to nonprofits over time. For recipient organizations, DAF gifts can be a lucrative funding source, but they also require careful reporting.

Understanding how to correctly report DAF contributions on Form 990 ensures compliance with IRS requirements, supports transparency, and builds trust with both fund sponsors and donors.

What is a Donor Advised Fund?

A Donor Advised Fund (DAF) is a charitable account managed by a sponsoring organization such as a community foundation, financial institution, or public charity. Donors contribute to the DAF, receive a charitable deduction, and can later recommend grants to qualified nonprofits.

It’s important to note that once a donor contributes to a DAF, the assets legally belong to the sponsoring organization, which has full control over how and when grants are distributed. For the nonprofit receiving the grant, this means the donation technically comes from the sponsor, not the individual donor. For compliance purposes, that is an important distinction.

DAF Contributions vs. Direct Donor Contributions

A key reporting distinction lies in whether the contribution comes directly from a donor or indirectly through a DAF sponsor.

| Source | How it’s reported | |

| Direct Contribution | Individual, business, or private foundation | Recorded as a direct gift from the donor |

| DAF Contribution | Sponsoring organization (for example, Fidelity Charitable, Schwab Charitable, or a community foundation) | Recorded as a grant from the sponsor, not the individual donor |

Even though the donor may have recommended the grant, the payment originates from the DAF sponsor, and because of that, your records should list the sponsoring organization as the donor.

When acknowledging the gift, nonprofits should issue the official tax receipt to the sponsoring organization, while also thanking the individual donor for their role in recommending the contribution.

Reporting DAF Contributions on Form 990

DAF-related contributions are reported on Part VIII, Statement of Revenue, under line 1 (“Contributions and grants”).

- Report on line 1f (“Other contributions”)

If the total amount received from a DAF sponsor meets the Schedule B reporting threshold, list the sponsoring organization (not the individual donor) as the contributor.

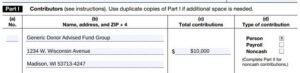

Example 1

If your nonprofit receives a $10,000 grant from Generic Donor Advised Fund Group (GDAFG) based on John Doe’s recommendation, report the gift as from GDAFG on Form 990 and Schedule B. John Doe should not be listed as the contributor.

Example 2

7 different donors contribute to GDAFG, and each recommends $1,000 to your nonprofit during the fiscal year. On Schedule B, your nonprofit should aggregate all gifts from GDAFG, in this case $7,000, and report the total as one contribution from GDAFG.

Nonprofits Sponsoring Donor Advised Funds

For nonprofits that maintain their own donor advised funds, additional details must be disclosed on Schedule D, Part I, including:

- The number of DAFs held

- Total contributions received

- Total grants made from those funds

- Year-end DAF balances

More DAF Best Practices

Beyond proper Form 990 reporting, nonprofits can strengthen DAF management through clear communication and coordination. Encourage collaboration between development and accounting teams so donor acknowledgments match up with financial reporting. Improper recordkeeping, like recording an individual as donor instead of the DAF, can lead to inaccurate financial reporting and other negative outcomes such as limiting contributions on your public support test when they may not have to be limited. Standardize acknowledgment templates to ensure the sponsoring organization is properly recognized while the recommending donor receives appropriate thanks.

It’s also helpful to educate staff about how DAFs work and to clarify that donor recommendations are not binding. Periodically review your acknowledgment language and donor database settings to confirm they reflect current IRS guidance and accurately track both the donor and sponsoring organization.

If your organization receives frequent DAF contributions or sponsors its own funds, reach out to the Wegner CPAs nonprofit tax advisors for guidance on maintaining accurate records and ensuring compliance with IRS reporting requirements.