Not-for-Profit (NFP) organizations typically receive support in the form of financial and nonfinancial assets to help achieve their missions. Nonfinancial assets include fixed assets (land, buildings, and equipment), the use of fixed assets or utilities, materials and supplies, intangible assets, services, and unconditional promises of those assets.

In September 2020, The FASB issued Accounting Standards Update (ASU) 2020-07, Not-for-Profit Entities (Topic 958): Presentation and Disclosures by Not-for-Profit Entities for Contributed Nonfinancial Assets. The purpose of the ASU 2020-07 is to clarify the presentation and disclosure of contributed nonfinancial assets with an intention to provide the reader of the financial statements a clearer understanding of what type of nonfinancial assets were received and how they are used and recognized by the NFP. It is important to note that the ASU 2020-07 will not change the accounting and recognition of nonfinancial assets but rather the presentation and disclosure requirements in the financial statements.

The presentation and disclosure requirements of the ASU are as follows:

Presentation Requirement

- Present contributed nonfinancial assets as a separate line item in the statement of activities, apart from contributions of cash and other financial assets.

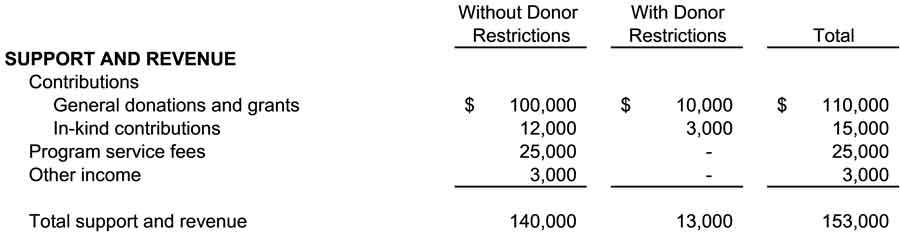

Example of Presentation Requirement

This provision is the only presentation requirement and has been implemented to provide a clear distinction between financial and nonfinancial assets received by the NFP. The following is considered the most common approach to presenting contributed nonfinancial assets on the statement of activities.

Separate Row Presentation

As shown above, the contributed nonfinancial assets (in-kind contributions) are separately listed under the “Contributions” heading as opposed to being grouped with the “general donations and grants” line item which may have been done in the past.

Disclosure Requirements

- A disaggregation of the amount of contributed nonfinancial assets recognized within the statement of activities by category that depicts the type of contributed nonfinancial assets.

This requirement provides the reader of the financial statements an understanding of the types of nonfinancial assets received. Categories can include broad terms such as “clothing” instead of listing out specific clothing items to avoid lengthy disclosures that contain unnecessary details.

- For each type of contributed nonfinancial assets recognized (as noted above), a NFP will be required to disclose:

- Qualitative information about whether the contributed nonfinancial assets were either monetized or used during the reporting period. If used, an NFP should disclose a description of the programs or other activities in which those assets were used.

- The NFP’s policy (if any) about monetizing rather than using contributed nonfinancial assets.

- A description of any donor-imposed restrictions associated with the contributed nonfinancial assets.

- A description of the valuation techniques and inputs used to arrive at a fair value measure, in accordance with the requirements in FASB ASC 820, Fair Value Measurement, specifically FASB ASC 820-10-50-2-(bbb) (1), at initial recognition.

- The principal market (or most advantageous market) used to arrive at a fair value measure if it is a market in which the recipient NFP is prohibited by a donor-imposed restriction from selling or using the contributed nonfinancial assets.

These requirements provide the reader of the financial statements additional information to enhance their understanding including how the contributed nonfinancial assets are being used in their program services or supporting activities as opposed to being liquidated, any restriction placed on the assets, and methodologies and determination of fair values.

Examples of Presenting these Disclosures

While all disclosures mentioned above for ASU 2020-07 must be made, there is no specific requirement for how the information is presented. The following are considered common approaches at presenting the required information.

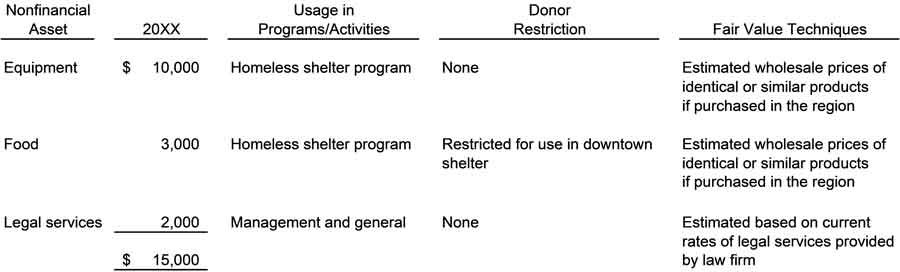

Tabular Presentation

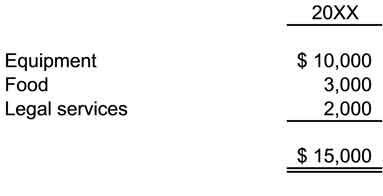

Narrative Presentation

In-kind contributions included in the statement of activities are comprised of the following:

Fair value techniques – Equipment and food are valued using estimated wholesale prices of identical or similar products if purchased in the region. Legal services are valued based on current rates of legal services provided by law firm.

Donor restrictions and use – Food is restricted for use in the downtown shelter. All other in-kind contributions are not restricted. The Organization does not sell in-kind contributions and uses equipment and food in the homeless shelter program and legal services in management and general activities.

Effective Date and Transition

The ASU 2020-07 should be applied on a retrospective basis and effective for annual periods beginning after June 15, 2021, and interim periods within annual periods beginning after June 15, 2022, with early adoption permitted.

Conclusion

The issuance ASU 2020-07 was developed to bring consistency of presentation and disclosure among NFPs for contributed nonfinancial assets. As with other requirements, consideration should be made as to significance or materiality when complying with the presentation and disclosure requirements of this ASU. Please contact your engagement in-charge at Wegner CPAs for any additional questions or to review the impact this may have on your financial statements.