What is ASU 2018-08 and will it Impact Me?

On June 21, 2018, the Financial Accounting Standards Board (FASB) issued Accounting Standard Update (ASU) 2018-08: Clarifying the Scope and the Accounting Guidance for Contributions Received and Contributions Made. This ASU will impact all organizations that receive or make contributions of cash or other assets. The only transactions excluded from this ASU are transfers of assets from government entities to businesses.

Summary of ASU 2018-08

This ASU includes specific criteria to consider when determining whether a contract or agreement should be accounted for as a contribution or as an exchange transaction. It also provides a framework for determining whether a contribution is conditional or unconditional which will impact the timing of revenue recognition. As a result of this new ASU, not-for-profit organizations will account for more grants/contracts/agreements as contributions, specifically conditional contributions.

Contribution vs an Exchange Transaction?

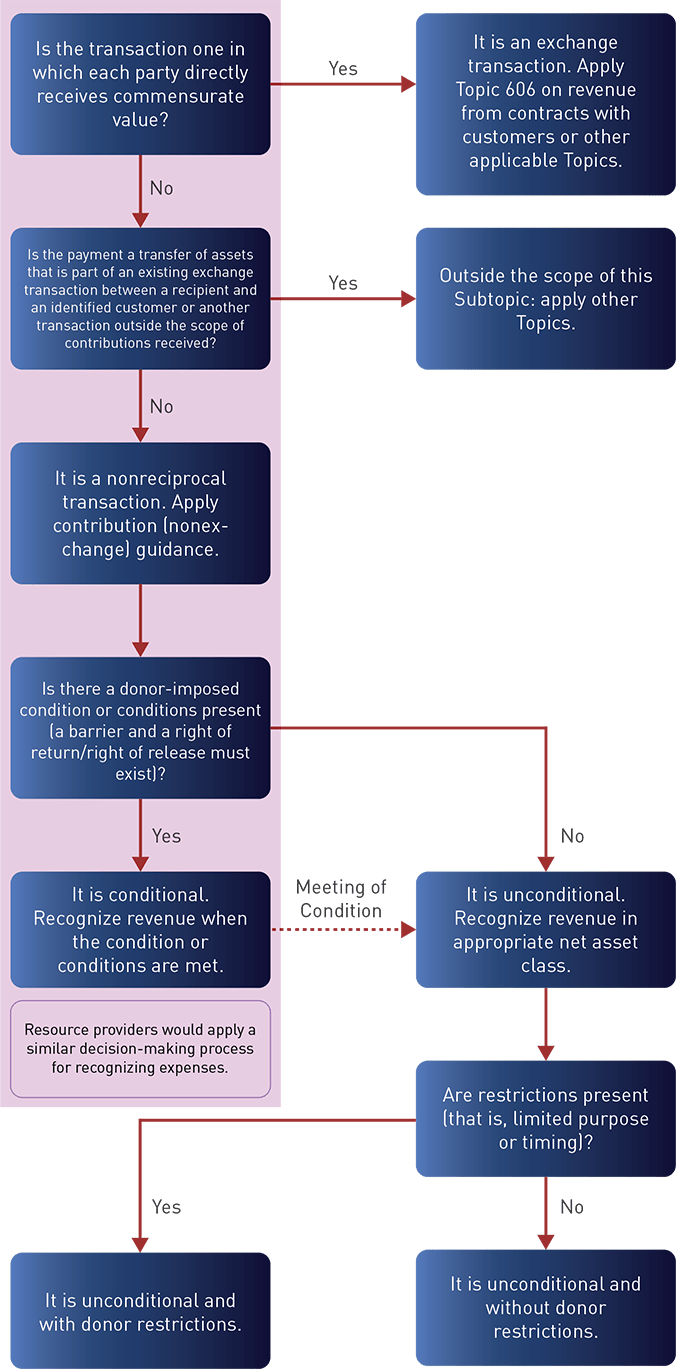

The determining factor for whether an organization will account for a grant/contract/agreement as a contribution or an exchange transaction is whether the asset provider is receiving commensurate value in return for those assets. If commensurate/proportionate value is received, it is accounted for as an exchange transaction and follows revenue recognition or other applicable standards. If commensurate value is not received by the asset provider, it is accounted for as a contribution and follows contribution standards. If some value but not commensurate value is received, then it is accounted for as both an exchange transaction and a contribution. A decision tree flowchart is included in ASU 2018-08 and can be found at the end of this article.

Examples

Example 1: If a City provides a grant of $5,000 for Entity ABC to conduct a study on the homelessness patterns in that City (approx. cost $5,000) and requires Entity ABC to provide the report, data and findings back to the City, this would be accounted for as an exchange transaction because the City (asset provider) received commensurate value for the grant.

Example 2: If the City provides a grant of $5,000 for Entity ABC to provide meals to the homeless in that City and requires Entity ABC to provide a quarterly report of number of meals served, this would be accounted for as a contribution. The City (asset provider) has received no direct benefit or commensurate value for the grant. Note: In this ASU, it is clear that societal benefit or benefit to the general public is not considered commensurate reciprocal value to the asset provider.

Example 3: If the City provides a grant of $10,000 for Entity ABC to conduct a study on the homelessness patterns in that city (approx. cost $5,000) and requires Entity ABC to provide the report, data and findings back to the City, this would be accounted for as both an exchange transaction and a contribution. There would be an exchange transaction recorded for the $5,000 in value that the City (asset provider) received and a contribution of $5,000 for the amount provided in excess of value received.

Example 4: If Medicare provides a Hospital with $7,500 for services rendered to Patient N, this is accounted for as an exchange transaction even though Medicare did not receive commensurate value. This is one of the exceptions found in the ASU. Per the ASU, this payment is actually a payment relating to an existing exchange transaction between the Hospital and Patient N. The key determining factor for this exception is that the patient/customer must be specifically identified in the agreement.

Conditional versus Unconditional Contributions

Once the organization has reviewed the grant/contract/agreement and determined that it is a contribution, the next step is to determine whether the contribution is conditional or unconditional. An unconditional contribution is recognized immediately whereas a conditional contribution cannot be recorded until the conditions have been met.

To be a conditional contribution, the grant/contract/agreement must include both of the following:

- A right of return to the asset provider or a right of release from the obligation to provide funds/assets (meaning that the asset provider has the right to get their funds back or not to release future payments on promises to give if the organization does not meet the conditions)

- One or more barriers need to be overcome before the organization is entitled to the assets transferred or promised

The ASU also provides some guidance in identifying barriers in the contract. There are three specific things to look for:

- Measurable Performance-Related Barrier or Other Measurable Barrier

- The organization is required to achieve a measurable outcome or a specific event must occur

- Examples – Serve 1,000 homeless per month, add 5,000 square feet to the facility, host 10 job coaching events for the unemployed, receive $100,000 in matching contributions in the next 3 months

- Limited Discretion on the Conduct of an Activity

- The organization has limited discretion over the manner in with an activity can be conducted

- Examples – Incurring qualified expenses, requirements to hire specific individuals or a specific protocol that must be followed

- Stipulations that are Related to the Purpose of the Agreement

- The organization has limited discretion over how the funds are used

- Examples – Funds must be used to expand facilities, funds must be used to purchase a piano, funds must be used for esophageal cancer research

If a right of return or right of release and one or more barriers are identified during the review of the agreement, the contribution is conditional and cannot be recorded as revenue until the barriers are overcome. If the transfer of assets occurs before the barriers are overcome, this should be accounted for as a refundable advance until the conditions have been substantially met or explicitly waived by the donor.

What is changing compared to the current standard and what do I need to know about implementation?

Under this new standard, every grant/contract/agreement must be analyzed under the new framework to determine if it will be recorded as a contribution, an exchange transaction or both. For any agreements identified as conditional contributions, the organizations will also need to identify and track the specific conditions of the contract and record the contributions as the conditions are met.

This ASU will be applied using the modified prospective basis. This means it will be applied to agreements that are not completed as of the effective date (only applies to the unrecognized portion) and to agreements that are entered into after the effective date. For most not-for-profit organizations, they should consider these new standards for any contracts they sign that will still be in effect as of December 31, 2019 or thereafter. No prior period results should be restated, and there should be no adjustment to net assets as a result of implementing this standard.

As a result of this new ASU, not-for-profit organizations will account for more contracts/agreements as contributions, specifically conditional contributions. Revenue recognition on conditional contributions is delayed until the conditions are met and therefore, in the year of implementation, not-for-profit organizations may see a drop in their revenue. In addition, conditional contributions must be disclosed in the footnotes. Overall, implementation of this new ASU will result in an increase of conditional contributions, a reduction of recorded unconditional promises to give, a reduction in reported temporarily restricted net assets and increased footnote disclosures.

Decision Tree Flowchart from ASU 2018-08